Everyone hates paying for laundry. If you’re lucky, it works like an old-school vending machine, where you feed in your card and it spits it back out and you’re ready to wash. If you’re not, you have to deal with getting rolls of quarters from the bank to feed into a coin drop that only works half the time, or, worst of all, an app. I held out for a long time against laundry apps. In college, I brought my laptop to the laundry room of my dorm to pay for washing and drying, using the clunky browser portal instead of downloading the app they wanted me to use.

There are lots of downsides, for the launderer, in using an app. For one, you have to download it and keep it on your phone. Usually they don’t work very well. Sometimes, landlords change which app you’re using, and all of a sudden the credit you put in (because they all require you to prepay) becomes worthless to you. And, apparently, they can advertise gambling to you.

My apartment uses PayRange to process payments for laundry services. To the people downloading their app, voluntarily or not, they’re a company that “lets you pay for vending, laundry, arcade, parking, coffee, and other machines with a simple swipe of your finger.” To their customers, they’re a “platform that enables cashless commerce and self-service retail with mobile technology.”

When I first moved to my apartment, I resisted downloading PayRange fiercely. The machines here still take quarters, and so I went back to the bank and picked up $10 rolls of quarters. Technically, using coins is cheaper, but I gave in when my roommate told me that you get a longer dry cycle if you pay digitally–$2.50, instead of $2, but 90 minutes instead of 45. And at first, when I downloaded the app, it wasn’t so bad. It worked reasonably well, although it required a distressing number of permissions, so I paid for my laundry the way my landlord wanted me to.

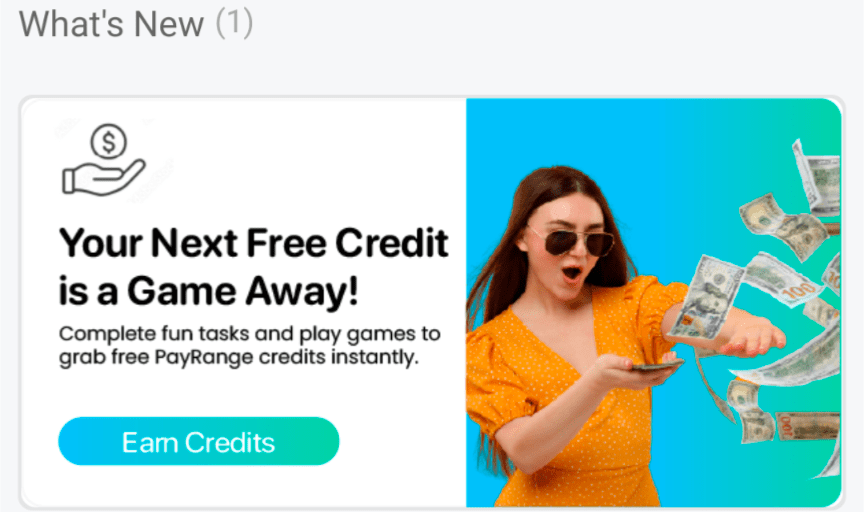

But then, I got a popup, telling me that I could get free credits if I played a game. I tapped on it, and I looked through the apps, standing in my apartment’s tiny laundry room on top of lost socks and balls of lint.

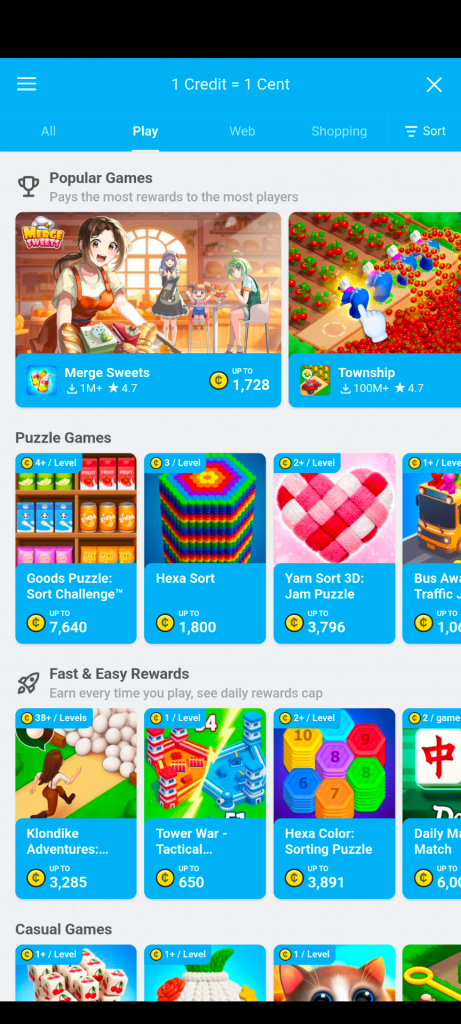

When you open the PayRange app’s games section, there are a dozens of mobile games immediately presented to you. It’s like a smaller version of the app store, with games sorted by their payouts, cost to play, and genre. Word City promises a maximum payout of $148.49, costing $0.01+ (whatever that means) per level. Other have more reasonable payout scales, offering payments of up to $3.00 at one cent per level. Many of the games seem to be purely chance based, although I have not played enough to find out. Technically, this isn’t gambling. There is no way to convert your vending-laundry-arcade-parking-coffee-other credits into cash. It resembles a video game lootbox, or one of the many “mystery box” services that popped up in years past, both of which skirt the line between “gambling” and “game”.

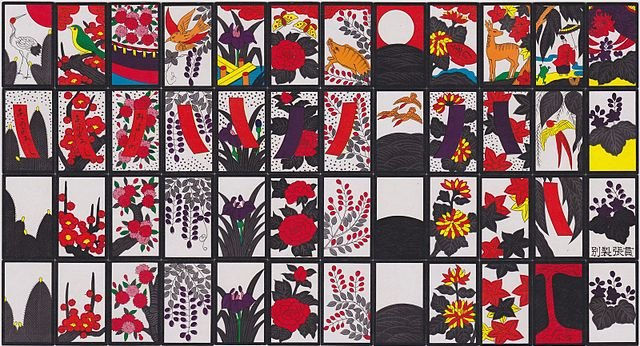

This has, of course, been a long tradition in the United States and the world. Gambling was once tightly-regulated in most parts of the country, which was the driver of the rise of Native American casinos, which were based on the Supreme Court finding that states could not regulate activities on reservations. Rook cards were invented by American puritans to make gambling “impossible”, and hanafuda playing cards—decorated with pictures of flowers—were invented in Japan so that gamblers could claim that they were simply looking at pictures. Neither were completely effective, and, in truth, where you have two people, cash, and something that could turn out one way or the other, there is always the ability to gamble.

I grew up relatively sheltered from gambling. I didn’t see my first ad for sports betting until I spent a summer living in Michigan in an apartment that happened to have cable included. Before that, I always thought of the practice as something carried out by bookies, hiding lists of bets under their coats and taking bets from anyone around them. Nobody in my family gambles, and when we visited Las Vegas as kids, it was to see the Grand Canyon and the Hoover Dam.

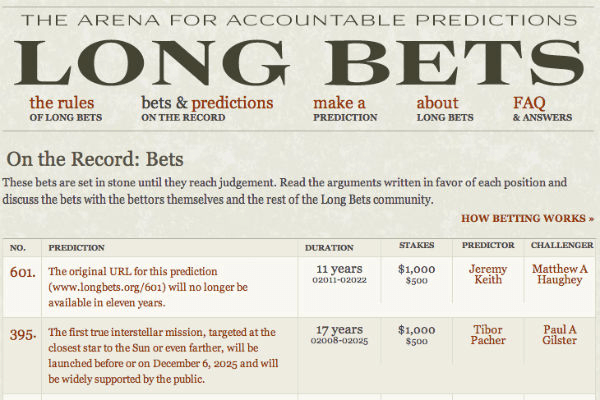

But, American society has changed dramatically. Sports betting was federally legalized in 2018, and this has led to a tight intermarriage between sports and gambling. At the same time, online future forecast betting went from an obscure game to a popular pastime. Long Bets, a nonprofit operated by the Long Now Foundation, was launched in 2002, or 02002 in the Long Now system of dating. Its objective was to encourage consciousness about the future and improve future predictions by having people bet on distant future events, at least 2 years from the time of betting. The money put into an investment account would be sent to the winner’s preferred charity. Neither player would receive money.

Long Bets have been outcompeted in their field by short-term prediction gambling sites like Kalshi and Polymarket, which allow people to bet on anything they like. One bet from the Long Bet site (https://longbets.org/9/) actually ended up using the Metaculus prediction market to resolve its bet.

Much has been said about these prediction market sites already, and I see no need to discuss it here. What is more concerning, I think, is the proliferation of gambling into more and more sectors of American life. Why would someone gamble with laundry money? I have not yet met anyone, online or in person, who says they have played the games. One of my friends did express interest in creating a bot to consistently and quickly win games to accumulate points once I mentioned it, although as far as I am aware he hasn’t gone through with it.

I think one possibility is that people might gamble for fun. My friend Emil gambles regularly, but he insists on never putting in much money. “They give you a hundred bucks to sign up, and a dollar every day,” he told me about the gambling site he was using. Then, I sat across from him in a Mexican restaurant and watched him play pachinko over and over. After about ten rounds, he’d used up his free dollar, and he put his phone away. A friend of mine hosted a Superbowl watch party this year, and only two people were paying attention. I was watching it because I’m a fan of the Seahawks, and Emil was watching it because he had money riding on the game. I can’t imagine that PayRange expects people to turn to it for gambling.

But there is a possibility that people might do it because it’s there. Recently, a lot of video game development has been focused on attracting “whales”—users who are willing to spend exorbitant amounts of money to master the game. Diablo Immortal is a high-profile example of this (https://gameworldobserver.com/2026/01/19/italy-to-investigate-diablo-immortal-and-call-of-duty-mobile-for-dark-patterns), but many video games rely on it entirely, especially in the mobile space. Most users spend almost no money, and don’t play for very long, but a handful of users spend massively, putting in tens or hundreds of thousands of dollars (https://expertbeacon.com/who-spent-the-most-money-on-diablo-immortal/). In the context of a laundry app, I find it hard to believe that people would be willing to put in that much money. But people do, for games that are not much more involved than those in the app. With money already available, from the pre-paid balance in PayRange, there are the makings of a system designed to attract and profit from these users.

The second possibility might be worse: what if a significant percentage of people can’t afford to spend $5 a week on laundry?

There’s been a lot of talk about a K-shaped economy (https://fortune.com/2025/11/07/what-is-the-k-shaped-economy-wealth-inequality-explainer/) and how the wealthiest support the consumer economy while the poorest struggle with simple expenses. And the symptoms of this are obvious. Basically any purchase lets you pay in multiple parts, on everything from DoorDashed Chipotle burritos to groceries to shoes. And some people need to split up their purchases like that to get by. If you can’t afford to do $5 worth of laundry a week, I can absolutely see someone putting in the bare minimum amount of money, or using the very last bit of their prepaid credit, to gamble and try and get enough to do laundry.

Of course, there are other options. The usual grifts, where you register accounts on sites or do surveys for a small amount of money. I didn’t check if this option at all. And, on a third tab, advertisements for products and subscriptions for everything from GFuel energy drinks to electronic fax services to razors.

I thought about both of these possibilities, while I was looking at the ad that popped up while I was trying to do laundry, in my apartment full of black mold, where my dishwasher has never worked. I think that the latter is more likely than the former. Whales are not always wealthy. Some people go into incredible debt to feed their gaming or gambling addictions. But I suspect that in my complex, there were more people gambling because they have to than because they want to. In-unit laundry, or in-home laundry, are more common in luxury apartments.

So far, I have not found any information about people playing the PayRange gambling games for any reason. It’s possible that this is a strange experiment by an out-of-touch company. But I see gambling everywhere.

And, staring at my phone in a cramped dark room with the option to gamble for laundry, I cannot shake the feeling that I am living through a catastrophe.

Leave a comment